Editor's note: the below blog post was originally sent as an email to our clients on March 16, 2020.

I have spoken and met with many of you over the past few weeks, but givenwhat's going on, I wanted to get a broader message out to each of you. As always, feel free to call me at 810-471-3732 or hit "reply" with any questions. Please also be aware that I have the technology to do videoconferencing,shouldyou prefer not to meet in the office! That said, stay healthy, and please continue reading.

As of the end of the day on Friday, March 13, the S&P 500 is down 16.09% for the year. We did enter official "bear market" territory earlier in the week (meaning a draw-down of 20% or more), and despite Friday's rally, it appears that we may not have yet seen the worst of it.

The question of the month so far is,"WhatshouldI bedoing?"

Spoiler alert: in most cases, the short answer is, "nothing".

To understand why you likely don't need to take action in the midst of a crisis, let's first talk for a moment aboutwhatwe've already done.

- we met in person to discuss your financial situation (for most of you, we met more than once)

- we identified your long-term goals and objectives, including your target retirement date

- we conducted a risk tolerance assessment using Riskalyze to determine an appropriate level of risk for your portfolio

- we set up your portfolio to reflect the above

- we talked about the normal range of potential outcomes, including "outliers" or "black swans" based upon historical market performance

- we automated as much of your financial life as possible to keep emotions out of it (i.e. we've established systems to pay down debt, set up automatic 401(k) or IRA contributions, and turned on automatic portfolio rebalancing)

In short, we've focusing on controllingwhatwe can control. And that'swhatI'd suggest we continuedoing.

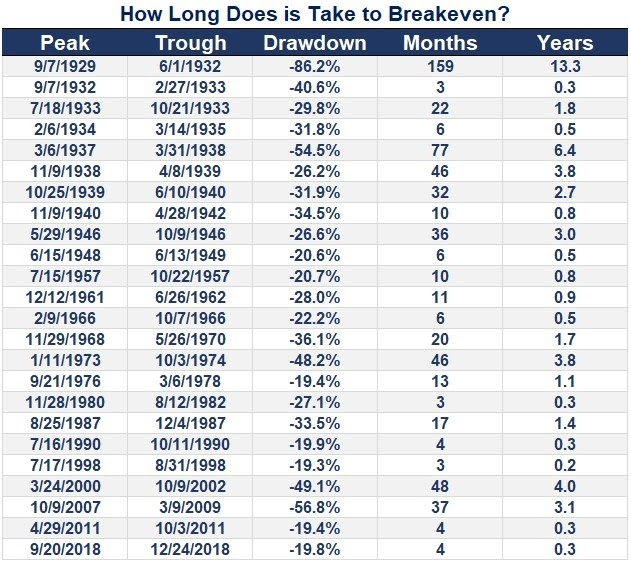

If you are currently retired or retiring within three to five years, you're likely more concerned than those with longer time horizons. Consider the below chart from Ben Carlson at A Wealth of Common Sense.

If you're a history buff, you may recognize some of those dates. The Great Depression, World War II, the dot-com crash, and the global financial crisis, to name a few.Whatthe data shows is that in the modern era (post-WWII), the average breakeven from a major drawdown was a little less than 17 months.

In other words, historically speaking, those who stayed invested andcontinued investingduring these downturns saw very high gains in the years that immediately followed to bring their portfolios back above and beyond their prior value. As Ben puts it, "every bear market in the history of the U.S. stocks has led to new all-time highs at some point in the future".

That is why "going to cash", "waiting it out", or "letting the dust settle" (also known as market timing) is typicallynotthe best approach.. because things can turn around quickly, and I want to make sure you're participating when they do!

Sowhatshouldyou bedoing? The answer is probably nothing. Still not sure? Give me a call.

We'll get through this, together.

Sincerely,

Marc R. Stasik, AIF®, MBA